After posting “Our Rules For Retirement,” my daughter replied “I guess I better get started working on not working!” I was immediately proud that she grasped the concept of the article as well as jealous that she encapsulated it so perfectly and succinctly.

Therefore, I had to steal her line as the title for this follow-up blog about retirement motivation and challenges. Plus, consider the real kicker of my daughter’s comment. If you are not “getting started working on not working,” then you are only keeping on working to keep on working… That sounds more like a voluntary form of slavery.

No one wants to be a slave, so why does anyone not simply just save up for their future? The big reasons are distractions, fear, and procrastination.

Distractions

Distractions provide the majority of the reasons people don’t save money. Some are fun distractions such as travel, parties, bigger houses, and fancy cars. In our life, my wife and I chose to spend more on our house and our kids and we chose not to spend on parties, fancy cars, or travel (at least, until we retired).

Naturally, some fun is required to enjoy life, but for those who don’t control their spending, these become a huge problem and lead to the no-fun distractions such as health issues or debt. Controlling spending and saving money for the future helps to manage bad luck (car accidents, bending one’s knee backwards playing basketball, etc.) as well as provide options for fun distractions in the future.

Fear

Many don’t know how to start or fear they will be bad investors. Especially with money managers often cautioning people that they “can’t do better than Wall Street, so why try?” Often the people parroting this information either profit from your belief or want you to assure them it is true so they don’t have to invest either.

The fact is that you don’t have to beat the market to have a financially secured future. In fact, you can make bad decisions and still do OK.

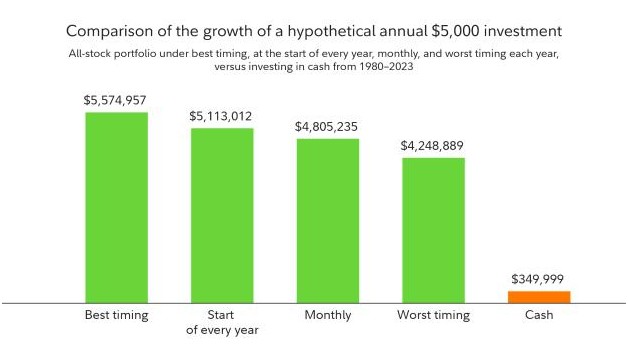

Fidelity Brokerage Services published an article in which they compared several different investing scenarios for a hypothetical person investing $5,000 per year in a Standards and Poor’s 500 Index Fund from 1980 to 2023. One interesting conclusion is that the very best investor and the very worst investor (from a market timing perspective) are not that far apart.

If someone invested (and held) all of their $5,000 annual investment at the absolute best time (lowest price) over the 40+ years, they would have $5,574,957. If someone messed up and bought at the absolute worst time (highest price), they would have $4,248,889.

Of course, everyone wants the extra $1.3 million, but $4.2 million isn’t a terrible retirement nest egg. Timing the market is very, very difficult to do correctly, so unless you spend a lot of time learning trading trends (a completely different skill), just get started.

Procrastination

Getting started is easier said than done and I have done my fair share of procrastination. I am also sure my young nieces and nephew are each thinking “I have lots of time before I am retirement aged.” While this is true, it is much easier to become successful using the power of compounding returns over time. In other words, starting with small amounts now, can lead to big results later.

But don’t worry about having all of your money to invest before you get started. Let’s look at the full chart from that Fidelity article:

In addition to the best and worst timing, we can see the power of compounding when we compare the total for holding cash ($349,999) against even the worst market timing ($4.2 million). Additionally, we can see that even if you don’t have the full amount of money to invest at the beginning of the year, which results in $5.1 million, a monthly investment that totals up to $5,000 overall for the year can still do quite well and generates $4.8 million in their example.

The $300k difference between the beginning of the year versus monthly investment shows the power of compounding still works over the short run, but not so much that you should beat yourself up about it. Invest what you can, when you can, and don’t worry about comparing against others.

Do You Have To Retire?

Do you have to retire? Of course not.

Some people love their jobs and staying in their job isn’t slavery, it’s fun. The real power of strong finances is not a pile of cash that allows you to just become a TV-watching blob. It is the options that money provides.

The option to stop working, the option to keep working, the option to change professions. Options can make our life easier and happier for every stage of life.

When starting out, money is the option not to be destroyed by bad luck (car accident, physical injury, etc.). As you get older, money is the option for big purchases (house, car, graduate school, etc.) or the option to change jobs with less worry for income disruption.

In retirement, one can still select the option to keep working. But it is always nice to have the option to walk away from a bad situation, either to a new job or into retirement because you have enough money in the bank.

The Finance Progression

In general investing should allow someone to progress through four stages:

- Stage 1: Work for money to live, paycheck to paycheck

- Stage 2: Work for money to live + savings (emergency funds, investments, etc.)

- Stage 3: Savings provide the money to live + Work for money to do other things

- Stage 4: Savings provide all the needed money and work is optional

Everyone goes through these stages. Some people get stuck and others can experience setbacks that force them to slide back.

I didn’t make nearly as much money consulting between jobs (7-8 years of my working career) as I did as an employee, so our stage 2 stalled for a long time. It wasn’t until we sold our house that we skipped stage 3 and went directly to stage 4. Even then, we were not confident about our income levels until almost a year later so we kept working as if we were in stage 3.

Get To Work On Your Future No-Job

In stage 4 of the financial progression, your savings becomes the “job” for your future self. By paying yourself early in life through saving and investing, you provide your future self with many more options.

Controlling your finances and debt can make progression between these stages easier and faster. However, that is a topic to explore in detail on another day. In the meantime, get working on not working! The alternative of voluntary wage slavery is just too sad.

Nicely done. The article was succinct, thorough and complete. Hope all readers can understand and implement successfully. P&G