My wife and I retired early and use our investment income to live. Whether they ever read it or not, this is the first of a series of articles for our kids, nieces, nephews, and friends that outlines how we achieved our financial independence.

The success formula, like the recipe for good health, is simple, but not necessarily easy to apply:

- Rule #1 Pay yourself first: live within your means and make saving a top priority.

- Rule #2 Put your money to work: select investments that will grow and compound.

- Rule #3 Avoid the Fat Tail of Risk: only make bets you can survive.

- Rule #4 Develop or borrow expertise: use pros until you develop your own knowledge.

- Rule #5 Harvest wisely: invest and sell investments to suit your needs for your stage of life.

Each of these topics will be expanded into a full article later to explain more details related to each rule. For now, I’ll quickly illustrate how we used these rules to create our financially secure future.

Rule #1 Pay Yourself First

We always made saving a priority. Of course we first had to pay for necessities such as rent, food, and medical costs. However, before we paid for entertainment or luxury, we put money aside to work for our future.

First, we paid off our debt, then we started with simple savings. We limited the number of times we went out to eat and didn’t buy alcohol, soda, pets, or expensive foods. We never had cable or satellite TV.

As we became more successful and were paid more, we first saved even more. Since we had not been spending money, it didn’t hurt to keep saving instead of spending the money.

But we didn’t become misers. After saving at least half of our new income we expanded our budget to allow a few luxuries such as more expensive meats, organic vegetables, and the basic tier of Netflix. But only after we fully funded our IRAs and 401ks.

Rule #2 Put Your Money to Work

We don’t leave our money as cash or bury it in the back yard. Instead, we continuously seek to improve the quality and the performance of our investments so they pay us back.

In the beginning, we started by investing in bank certificates of deposit (CDs), mutual funds, and exchange traded funds (ETFs). Later, we found other investments that we believed would be a better use of our money and invested in a variety of stocks and bonds.

Sometimes we were right and sometimes we were wrong (see rules #3 and #4), but we always had the majority of our money put to work. While this is a small sample of the types of available investments that will be covered some other day, the actual investment is less important than simply starting to invest as early as possible.

Even on the lowest-return investments (money market funds, CDs) compounding interest adds up and helps the “future you” to have more funds available. Even now, we can find value in the basic investments and use them when they make sense. But the most important part, was to start early, and keep improving.

Rule #3 Avoid the Fat Tail of Risk

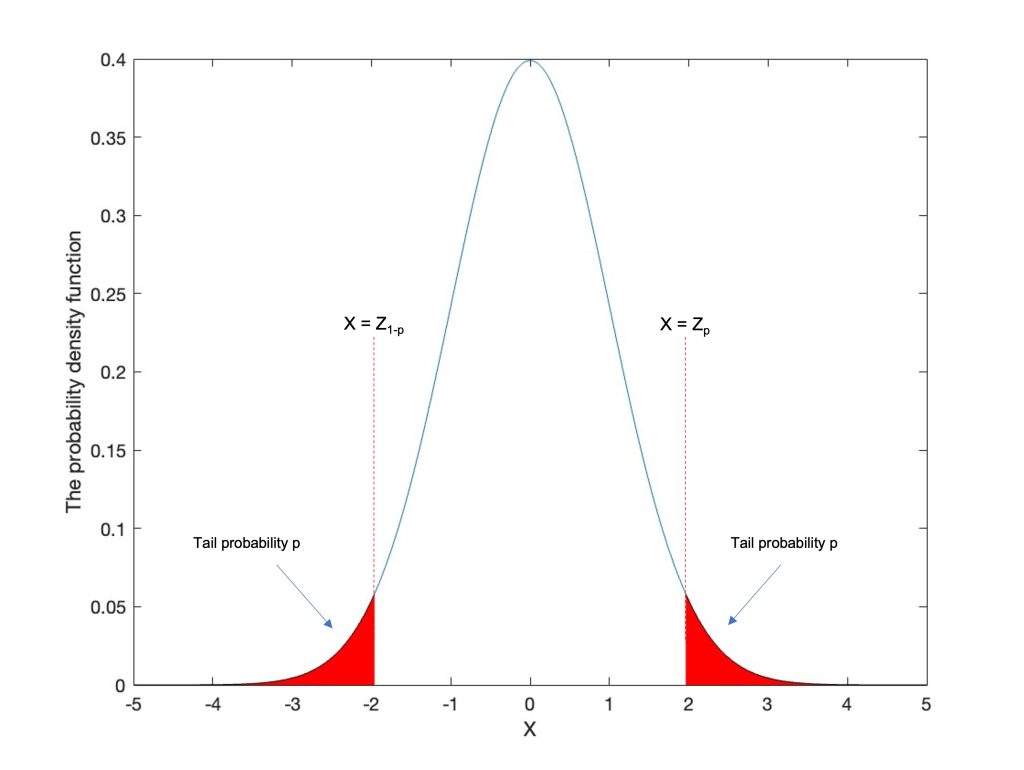

The “Fat Tail” risk is a strange concept for those that don’t know statistics. But it is easy to understand. Consider the following picture of the Normal Curve of statistics.

This function is normalized which means divided by the actual probabilities to give a generic version that works for almost all situations. The ‘tail’ probabilities, in red, are very unlikely and all of the probabilities under the center of the curve are the most likely.

For example, if you throw a ball of paper at a large trash can from next to it, it is very likely that your paper will land in the trash can (the center of the probability curve). There is a small chance that the paper will fall outside of the trash can (the tail probability, or red part of the curve).

The “Fat Tail” concept multiplies the risk by the pain of failure. In the paper thrown in the trash can example, the damage of missing the trash can is nearly zero, so the pain is also zero. No fat tail.

But on the other hand consider riding in a car without a seat belt. The risk of a car accident will vary depending upon street and driver conditions, but the risk of an accident should still be low. This is the red section of the curve.

Yet with no seatbelt, if the small probability event (the accident) occurs, you and other people could die (the maximum penalty). This is a fat tail event because even a small probability can result in maximum pain.

When investing, we can apply investing “seatbelts,” such as diversification of the types of our investments, to manage risks and minimize how painful any single mistake will become – no matter how confident we are in any one decision. We understand that we have a chance to lose all of our money in any single investment and many different investments (diversification) will still keep our financial future solid.

More specifically, we don’t have more than 20% of our money in any single stock and we buy a variety of investments (bonds, stocks, etc.) to lower risk. Even within stocks, we buy from different industries (energy, tech, healthcare, etc.) so that any mistake or market crash will affect only a portion of our investments.

Rule #4 Develop or Borrow Expertise

When starting out, put your money in the hands of experts until you can learn your own expertise. When we started, we bought CDs (bank expertise) and mutual funds or exchange traded funds (managed by stock experts).

To develop expertise, we started with small purchases of stock. This minimized our risk in case we were wrong (see rule #3) and allowed us to gain knowledge and experience. A few hundred dollars can seem like a lot of money to lose if you pick poorly, but it is a small tuition cost for a lifetime of learning.

Rule #5 Harvest Wisely

There are very few investments that will be the best option for you your entire life. Your needs will change dramatically over time and you may have opportunities that require you to sell one investment to buy another.

For example, we sold some of our investments and pulled money out of our retirement accounts to buy our first home (a condominium). We needed to stabilize our rent and needed more space for our growing family. After a few years, we saw an opportunity to sell the condominium and buy a home to give us even more space and higher rated local schools.

However, we never sold simply because the market was down or because the market was up. We invested intentionally based on strong knowledge of ourselves, our needs, and our objectives. In the last decade, for example, we started switching from high growth stocks to dividend paying stocks because we knew we would need the income to pay for our bills in retirement.

You Probably Have Questions?

These are a very high-level and vague set of rules, so you probably have quite a few questions. I will guess at some questions as I write more to explain each rule, but feel free to send me questions so I can explain these rules even better!

Why Should You Care?

If you look around, you can see that most people don’t retire early. So why should you care about early retirement?

You might be one of the few lucky people who love their jobs AND the people they work with AND the company they work for. Financial security means you have options and options means choices.

You can choose to quit working and travel while you are younger and have unlimited vacation days. Or, you can choose more income from continuing employment and increase your spending on nicer trips or nicer cars.

Without financial security, you will have more stress and more worries. The thought of you stressing throughout your life makes us sad, so we hope you will be willing to learn enough to be financially strong.

[…] starting to Pay Yourself First, cash starts to accumulate. That is when we Put Our Money to Work (our rule for early retirement #2), but to do so, we must pick both an investment and an account […]